RATES

As anticipated, the Federal Reserve made its second rate cut of the year on November 7, cutting rates a 1/4 point continuing the correction away from high borrowing costs. Mortgage rates dipped slightly following the announcement. November’s economic data will play a key role in the December announcement, potentially confirming analysts’ predictions of another rate cut. President-elect Trump has said he is looking to have more influence over the Fed and interest rates during his presidency. Historically, however, the Federal Reserve has operated independently from presidential administrations, and has made no indication that this approach will change going forward. Read more here.

NATIONAL MARKET

Gary Keller recently presented data on existing trends in the real estate market, addressing concerns that often surface in everyday conversations about the market’s health. While it’s true the market has shifted from peak levels a few years ago, the charts below reveal that, when viewed through a longer-term lens, the market is healthier than one might think.

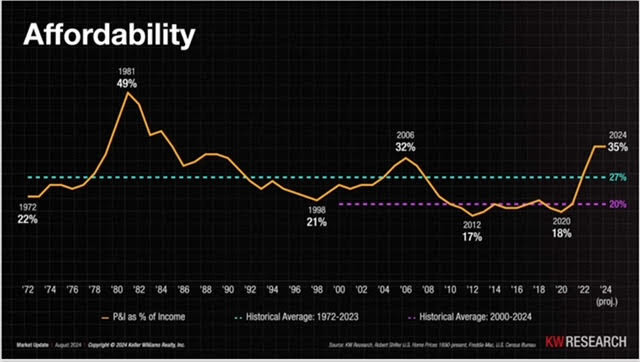

Many believe they’ll never be able to afford a home. However, we are currently only about 8% above the long-term trend when we look at the historical average of homeownership costs as a percentage of household income.

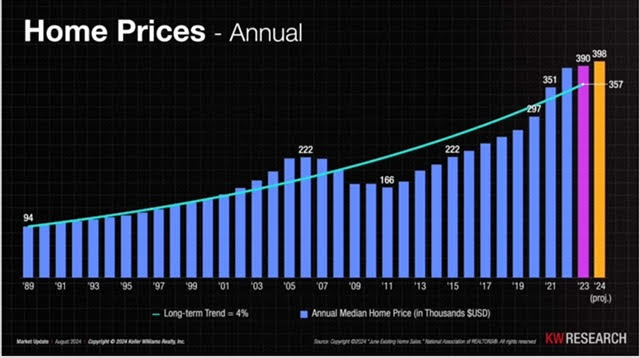

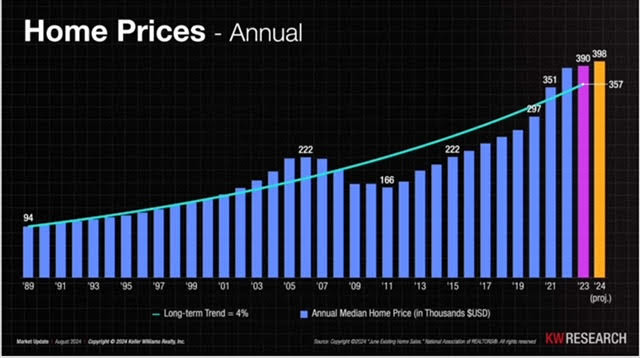

Many believe prices are at an all-time high. While prices are indeed elevated, they are currently only slightly above the long-term trend of 4% annual appreciation. Prices feel high because, from 2007 to 2020, they remained well below average.

Many believe mortgage rates have never been higher. While current rates are in the high 6’s to low 7’s, they are actually about one percent below the long-term historical average and less than a percent above the 25-year short-term average.

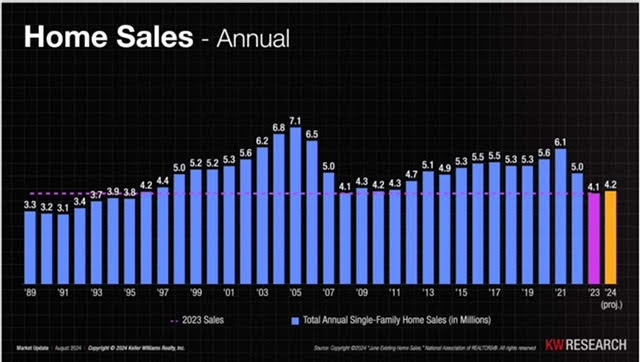

Many believe inventory has never been this low, currently hovering around 30% below healthy market levels. As shown in the chart above, this trend has repeated in a cyclical pattern over time dating back to the 1980s.